What is a Loss Run Report

By SortSpoke

Walk through any insurance industry conference in 2026 and you will hear the same story. Stock carriers issue AI strategy statements on earnings calls. Trade press covers autonomous agents. Vendors pitch end-to-end platforms. The implicit message lands the same way every time: there is a race to autonomous AI, the carriers ahead of the race will own the next decade of underwriting, and mutuals are behind.

The framing is wrong. The race that is being described is a race stock carriers are running for their own reasons — reasons that have more to do with quarterly earnings calls and analyst expectations than with combined ratios or member service. Mutual carriers are not running that race because they should not be. The structural facts about how mutuals operate make a different race the right one. And on that race, the math favors you.

This post lays out three structural advantages public carriers cannot replicate, the data that confirms mutual leaders already feel the inversion, and what to do next if you are in a position to act on it.

Public carriers operate on a quarterly clock. Earnings calls demand an AI strategy headline. Analyst reports demand pilot programs to point at. The pressure is structural, and it produces a particular kind of AI investment: visible, story-friendly, and often optimized for what the next earnings call needs more than what the business actually requires.

Mutuals do not have that pressure. The capital is patient. There is no quarterly story to tell. There is no analyst report to manage to. Mutual leadership teams can invest in execution rather than optics — and the difference between execution and optics is exactly the difference between AI that performs in production and AI that wins a press release.

This is not "be slow." It is "be deliberate." The 12-month-ROI rule still applies — if you cannot point to a measurable outcome within a year, you are funding research and development, not deploying production AI. The difference between mutuals and stock carriers is not pace. It is what each can credibly fund. Mutuals can fund the right thing. Stock carriers often have to fund the visible thing.

"Those carriers have R&D budgets you don't. Beat them at HITL execution, not at agent demos."

— Jasper Li, NAMIC Webinar, May 2026

The durable advantage is straightforward: while stock carriers fund expensive autonomous-agent experiments that will not see production for years, mutuals can build the human-in-the-loop playbook that is already working today. By the time the autonomous race resolves one way or the other, the mutual playbook is mature, in production, and compounding.

Mutual members are not just customers. They are owners. The capital at risk in an AI accident is not abstract shareholder capital — it is member surplus, the same surplus that protects them when losses spike and the same surplus the board has fiduciary responsibility for. That changes three things about how AI should be deployed in mutual carriers.

First, it changes what mutuals can credibly claim about responsible AI. When a stock carrier says they are committed to responsible AI, the structural alignment is weaker — shareholders ultimately want returns. When a mutual says it, the structural alignment is genuine: the people the AI serves are the same people the surplus protects. That is real credibility, not borrowed.

Second, it changes what regulators want to hear. Admitted carriers know this from experience — regulators are increasingly skeptical of autonomous decisioning, especially in lines of business where consumer protection or market conduct comes into play. Mutual structure gives regulators a story that lines up: ownership and accountability are aligned, decisions are auditable, humans remain in the loop on judgment calls.

"Don't gamble member surplus on an unsupervised agent."

— Jasper Li, NAMIC Webinar, May 2026

Third, it changes what is at stake in an AI accident. The asymmetry is structural. When autonomous AI goes wrong at a stock carrier, the cost is absorbed by shareholders. When it goes wrong at a mutual, the cost falls on the people the mutual exists to protect. That asymmetry is a feature, not a constraint — it forces the right architectural choices upfront. Human-in-the-loop is not a compromise here. It is the structurally correct posture.

Farm. Church. Contractor. Regional commercial. Specialty surplus. Mutual specialty appetites are narrow and document-heavy, and they almost never look like the standardized commercial monoline books that off-the-shelf "AI for submissions" platforms were designed around. That is not a constraint on AI strategy — it is, again, a structural advantage.

The reason: standard ACORD straight-through processing was built for vanilla books. For the documents mutuals actually underwrite — custom supplemental applications, specialty SOVs, multi-page loss runs with regional carrier formatting quirks, ACORD variants that no two brokers prepare the same way — straight-through processing breaks down. The right architecture for these documents is human-in-the-loop, where the AI does what it can and the underwriter makes the final call.

The carriers that struggle with this are the carriers that try to force-fit a big-carrier playbook onto a specialty book. The carriers that win are the ones that recognize the specialty appetite is the source of the advantage and match the technology to it.

Specialty models also drift faster than vanilla ones. Narrow appetites + changing broker behaviors + niche document evolutions = more vectors for drift. Mutual carriers running specialty books have to understand AI drift specifically because their books are more drift-vulnerable than monoline carriers' books.

"HITL is the strategy. Not a compromise."

— Jasper Li, NAMIC Webinar, May 2026

The carriers that win in specialty are the carriers that accept this as a structural fact, not a temporary state to be solved by the next generation of model improvements. The exception economy is the operating reality, and human-in-the-loop is how working teams run it.

The three structural advantages above are the argument. The data is the evidence. During Jasper Li's NAMIC webinar in May 2026, two polls of mutual carrier leaders confirmed what the structural argument predicts.

Source: NAMIC webinar poll, May 2026. Respondents: mutual carrier leadership and underwriting executives.

This is the single most important data point in the conversation. Zero percent of the mutual leaders in the room were all-in on autonomous AI. Fifty-four percent were already scaling — with humans in the loop. The race-to-autonomous narrative is not a description of what mutuals are doing. It is a description of what some stock carriers are saying they are doing, and the two are different things.

Source: NAMIC webinar poll, May 2026.

This second number inverts the usual B2B SaaS playbook. The dominant constraint for mutual leaders is not money. Capital is dead last. The dominant constraint is trust in the vendor — and behind that, sovereignty over data and models. The buying conversation for mutuals is not "convince me this is affordable." It is "convince me this vendor will not screw us in three years."

Both data points line up with the structural argument: mutuals are not behind on AI because they have rationally responded to the actual operating environment they live in.

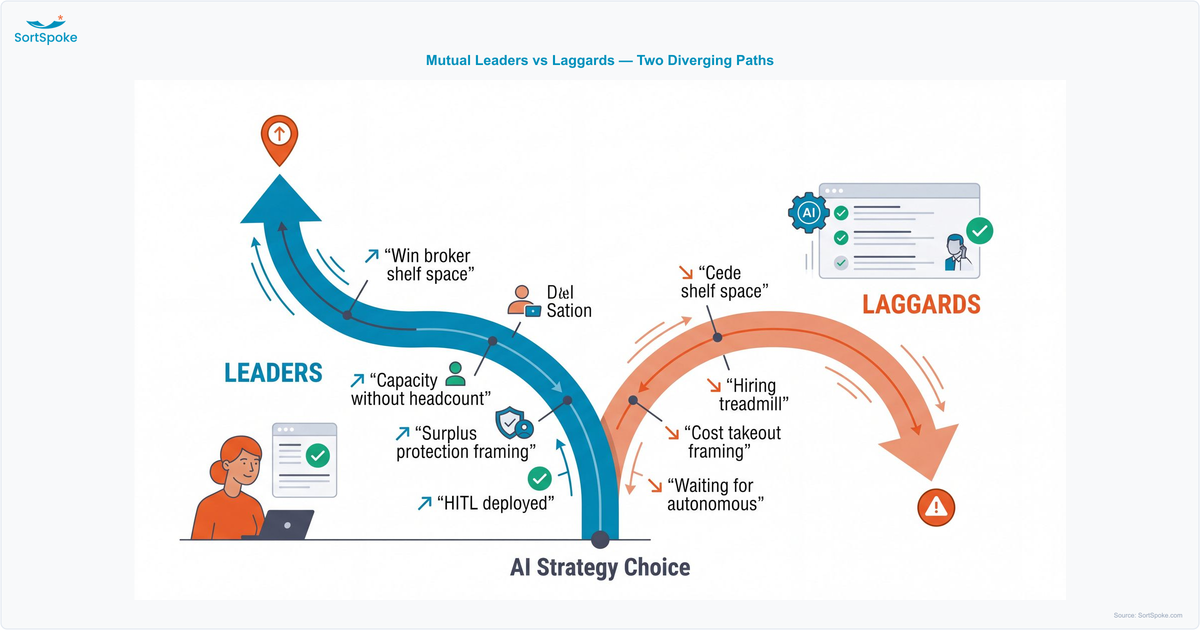

The structural advantages above are available to every mutual carrier. Whether a given carrier turns them into a real advantage depends on the strategic choices made over the next two to three years. The pattern is becoming clear.

| Mutual leaders will: | Mutual laggards will: |

|---|---|

| Deploy human-in-the-loop AI to scale capacity without growing headcount | Wait for autonomous AI to "mature" — stay on the hiring treadmill |

| Match tools to book complexity (HITL over STP for specialty) | Force-fit a big-carrier STP playbook, miss on niche risk |

| Frame AI as surplus protection and member service | Frame AI as cost takeout only |

| Win broker shelf space with response time and reliability | Cede shelf space, quietly shrink |

| Stay independent | Get demutualized or absorbed |

The last row is the one that should matter most. The failure mode for a mutual that cedes broker shelf space and stops keeping up with operational expectations is not "we are slower than we used to be." The failure mode is demutualization, absorption, or quiet decline into irrelevance. The strategic stakes are existential, not operational.

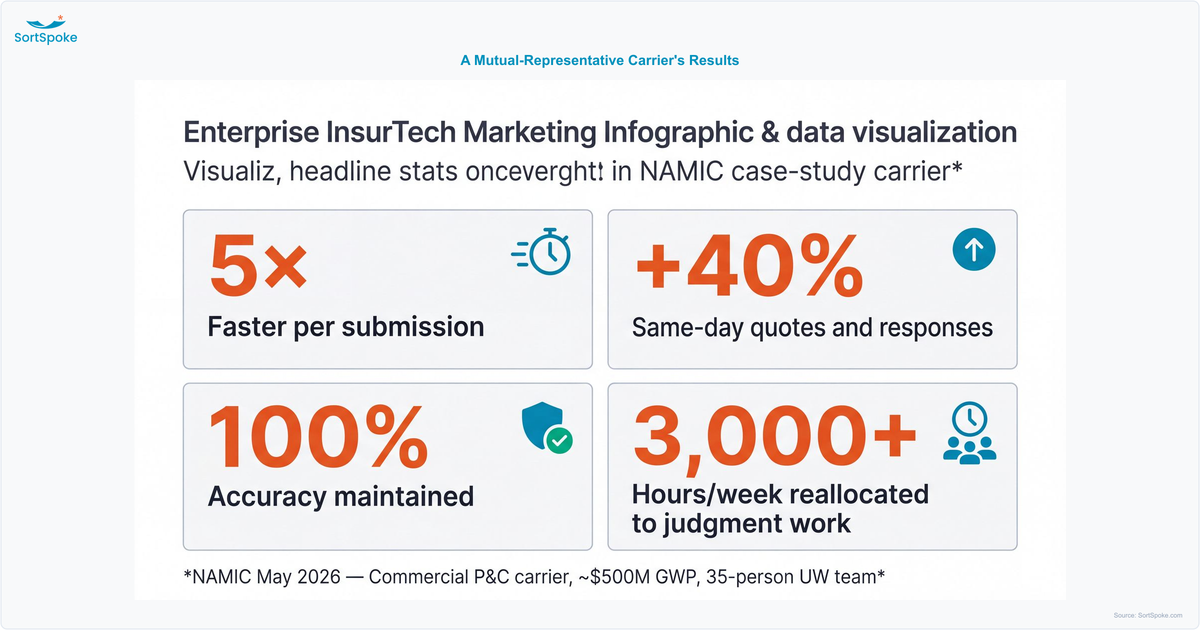

What does the leader path actually look like in practice? During the NAMIC webinar, Jasper shared the story of a commercial P&C carrier of mutual-representative size — around $500M gross written premium, a 35-person underwriting team, and 1,000 submissions per week. Volume was growing faster than headcount.

What they chose:

What changed within twelve months:

Source: NAMIC May 2026 case study. Commercial P&C carrier of mutual-representative scale.

None of those outcomes required betting on autonomous AI. None of them required ripping out core systems. None of them required a multi-million-dollar capital expenditure that did not fit how mutuals fund things. They required matching the technology to the book complexity, deploying human-in-the-loop where the work actually was, and naming the underwriters who would use it.

If the structural argument lands and the data confirms it, the question is what to actually do. Five practical principles, each grounded in the structural advantages above.

None of this is novel. The carriers winning at AI in 2026 are doing all five. They just are not the carriers issuing the press releases.

See how SortSpoke is built for the way mutual carriers actually operate. Visit the mutual insurance solutions page →

Or book a mutual-specific demo and we'll walk through what this looks like for your book, your specialty appetite, and your funding model.

Related reading: Why the Best Insurance AI Keeps Humans in the Driver's Seat covers the HITL pillar in depth. 9 Questions Before Buying Underwriting AI is the vendor-evaluation checklist. And AI Is a Plant, Not a Clock explains why specialty models in particular need ongoing care — and what to budget for it.

Commercial P&C Insurers Guide to Solving the Underwriting Bottleneck

.png?width=500&height=300&name=Website%20Blog%20Images%20(20).png)