The Exception Economy: Why Insurance Document Processing Will Never Be Fully Autonomous

By Brandon Robinson

Published December 12, 2023 | Updated March 4, 2026

The insurance industry's talent problem gets framed as a hiring problem. Open roles, unfilled seats, competition for candidates—it's all true, and it's all incomplete.

The harder truth is this: when a senior underwriter with 25 years of experience retires, they don't just leave an empty chair. They take with them an irreplaceable understanding of how to read between the lines of a complex submission—the judgment calls, the pattern recognition, the institutional memory that no job description can capture.

The talent crisis is really a knowledge crisis. And solving it requires a fundamentally different approach than posting more job listings.

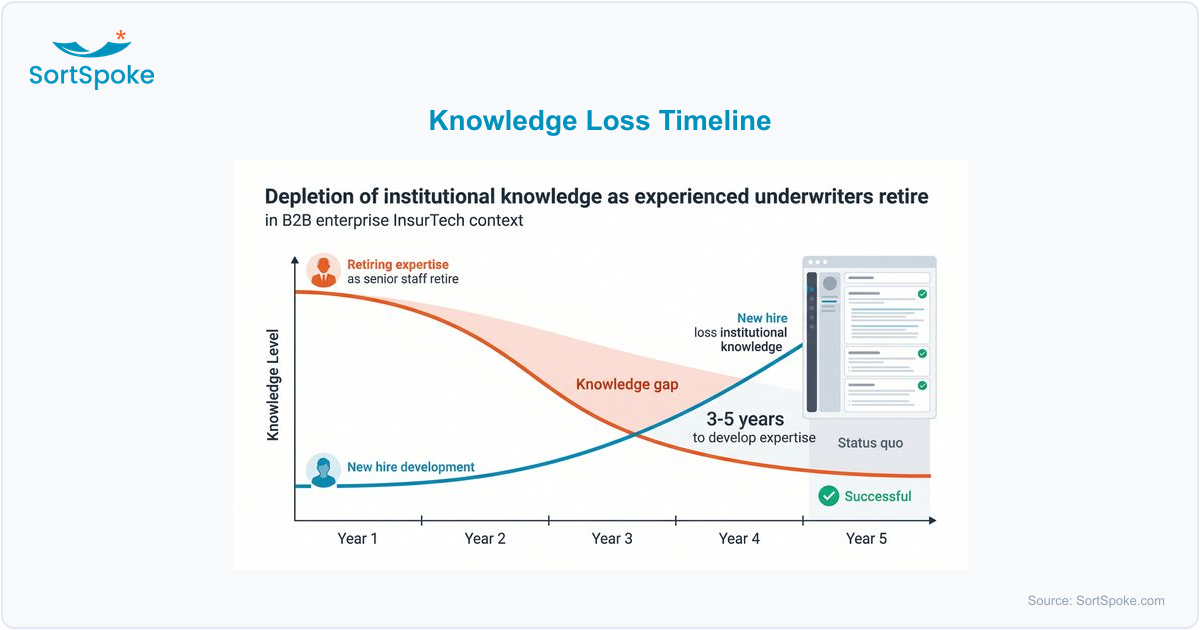

The numbers are stark. An estimated 400,000 insurance professionals will leave the workforce by 2026, driven primarily by Baby Boomer retirements. In commercial P&C underwriting specifically, this means carriers are losing the people who built their books of business, who know how to interpret ambiguous risk data, and who've developed the judgment that only comes from decades of experience.

Meanwhile, the pipeline of replacements isn't keeping pace. Younger professionals entering insurance often gravitate toward InsurTech startups or other industries entirely. The ones who do join carriers face a steep learning curve—commercial underwriting expertise typically takes 3-5 years to develop, and that assumes access to experienced mentors who have time to teach.

When one senior underwriter mentors two juniors, that's manageable. When three seniors retire in the same year and you need to onboard five new hires simultaneously, the math breaks. Your remaining experienced staff are now split between doing their own work and training replacements—and both suffer.

Most carriers are addressing the talent gap with some combination of competitive compensation, university recruiting, and training programs. These matter—but they don't solve the core problem.

You absolutely need to recruit. But hiring a smart, motivated person doesn't mean they can interpret a complex financial statement the way your 20-year veteran can. The knowledge gap between "technically qualified" and "genuinely expert" is measured in years, not training modules.

Procedure manuals and SOPs document what to do. They rarely capture why an experienced underwriter makes a particular call—the subtle signals in a loss run that suggest a risk is deteriorating, or the patterns in a financial statement that indicate a business is more resilient than the numbers suggest.

Fully automated solutions that remove human judgment from the process aren't the answer either. Commercial underwriting involves ambiguity, context, and nuance that most AI systems can't handle reliably on their own—which is why 78% of AI pilots in insurance never scale to production.

The carriers that are navigating this transition most effectively have shifted their framing. They're not just asking "How do we fill seats?" They're asking "How do we preserve and scale what our best people know?"

This is where human-in-the-loop AI becomes a knowledge transfer mechanism, not just a productivity tool.

Human-in-the-Loop AI for Knowledge Transfer

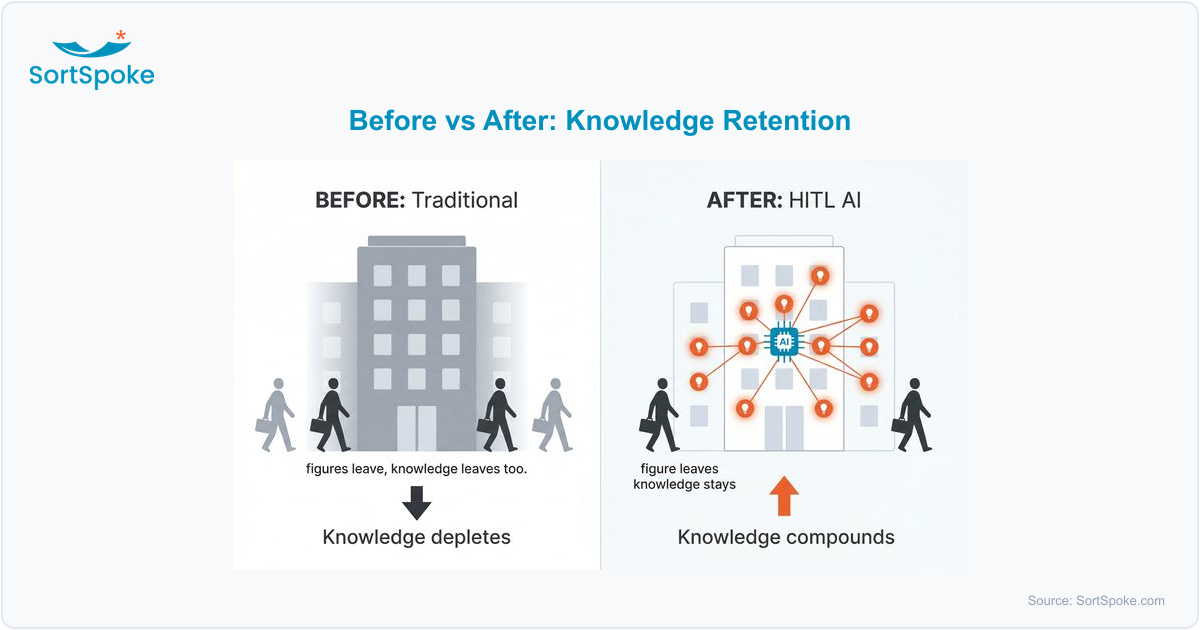

Human-in-the-loop (HITL) AI systems are designed so that human experts review, correct, and validate AI outputs. In underwriting, this means your senior staff teach the AI how to interpret complex documents—and the AI retains that knowledge permanently, applying it consistently across every future submission.

Here's what this looks like in practice:

The result is an organization where knowledge compounds instead of depleting. Every month the system runs, it knows more—the opposite of what happens when experienced people leave a traditional operation.

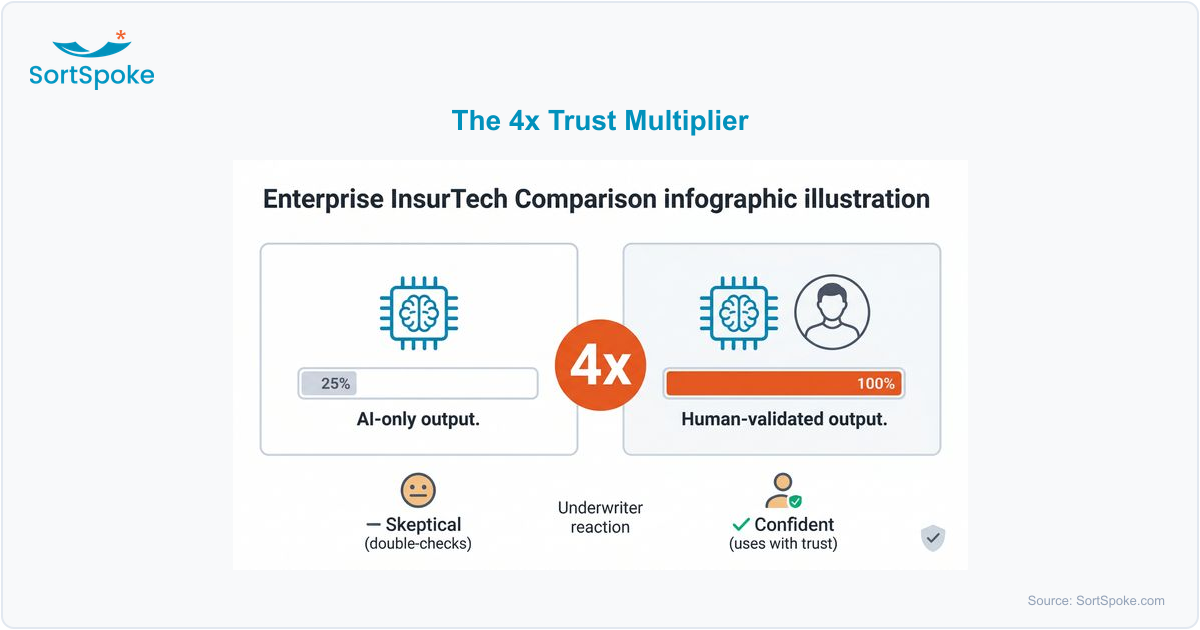

One of the underappreciated benefits of keeping humans in the loop is what it does for trust—both from the underwriters using the system and from the organization making decisions based on its outputs.

Research on AI adoption in insurance shows a striking pattern: underwriter trust in AI outputs increases by 4x when human review is part of the process. When people know that an experienced colleague has validated the data, they use it with confidence. When they don't, they double-check everything manually—eliminating the efficiency gains the AI was supposed to deliver.

This matters enormously for the talent crisis. If your new hires don't trust the tools, they'll revert to manual processes. If your senior staff feel the AI is undermining their expertise rather than amplifying it, they'll resist adoption. Augmentation—not automation—is the approach that actually sticks.

The practical path from "losing knowledge" to "compounding knowledge" follows a pattern we see across carriers:

Start with the documents where your senior underwriters add the most interpretive value. For most commercial P&C teams, that's ACORD forms, financial statements, or loss runs. Deploy intelligent document processing and have your experts review and correct the AI's outputs.

As the AI learns from corrections, accuracy climbs rapidly. The system typically reaches production-level reliability within 50-75 documents. Your senior underwriters shift from correcting most outputs to spot-checking exceptions—freeing their time for mentoring and complex risk assessment.

Expand to additional document types. By this point, new hires can process standard submissions with AI assistance from day one, while the AI preserves the judgment patterns of your most experienced staff regardless of whether those individuals are still on the team.

Knowledge preservation is the strategic rationale. But the near-term business results are what fund the investment:

These aren't theoretical projections. They're the results carriers are seeing when they approach the talent challenge as a knowledge architecture problem rather than a pure recruiting problem.

If the talent crisis is already affecting your team, the worst response is to wait for the perfect strategy. The best response is to start capturing knowledge now, before your most experienced people leave.

The practical first step: identify the one document type where your senior underwriters add the most interpretive value, and deploy a human-in-the-loop document AI solution against it. In 30 days, you'll have measurable results and a clear picture of what scaling looks like.

Ready to see how your team can preserve underwriting expertise while boosting capacity? Book a demo →

Commercial P&C Insurers Guide to Solving the Underwriting Bottleneck

Related articles