What is a Loss Run Report

By SortSpoke

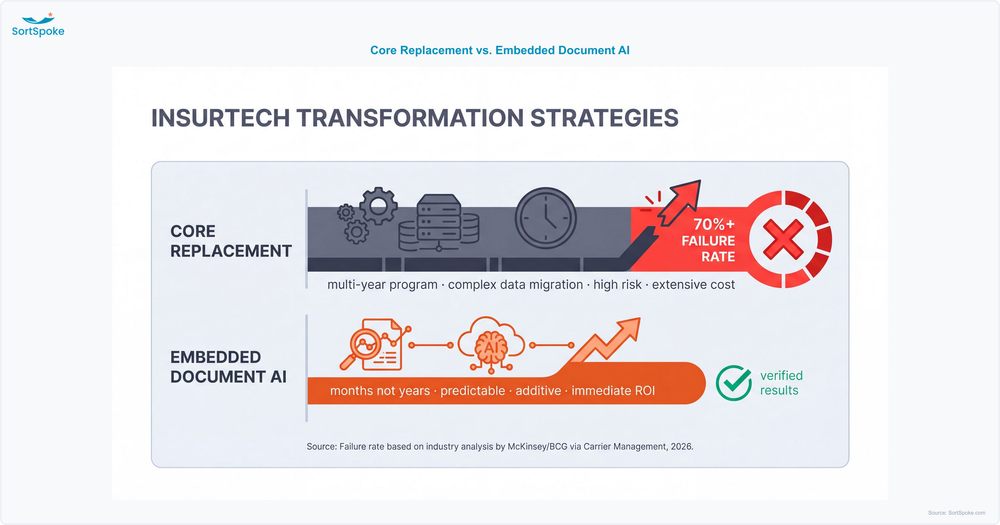

Seventy percent of large-scale core insurance system replacements fail, stall, or quietly run alongside the very system they were meant to retire. Roughly one in four becomes a complete write-off. At a January 2025 Datos Insights session on core transformation, one industry leader disclosed an implementation that had been running for fifteen years. The math behind insurance legacy system modernization hasn't worked for a decade — yet for most of that decade, the playbook didn't change.

It's changing now. The carriers actually moving the needle in 2026 aren't betting the roadmap on replacing Guidewire, Duck Creek, or Sapiens. They're keeping the core thin and adding intelligence at the edges — where submissions arrive, where documents get read, where brokers wait for answers. This post lays out that architecture, the buyer's test that screens any AI pitch in a single question, and the honest cases where replacement is still the right call.

Start with the numbers, because they're the whole argument. According to research from both McKinsey and BCG cited by Robert Pick — Group Deputy CITO at Tokio Marine — in Carrier Management, large-scale core system transformations fail more than 70% of the time, and almost a quarter of the time they become full write-offs. Gartner puts the share of data-migration projects that fail outright or blow past budget and timeline at 83%, with overruns averaging roughly a third on cost and 40% on schedule.

This isn't a technology problem. The platforms work. It's a strategy problem — a decade-long pattern of carriers choosing the single highest-risk modernization path available and then discovering, mid-program, that the new system can't replicate everything the old one quietly did. Practitioners call the result the "dual-system trap": you can't complete cutover, so you run both platforms indefinitely, paying twice and modernizing nothing.

Pick frames the alternative as "modern enough" — a system that is integratable via APIs, secure, functionally sufficient without manual workarounds, vendor-supported, cost-effective, and well-documented. His line is the one every architect should tape to the wall:

"Every dollar/euro/yen spent replacing something that already works is capital NOT spent advancing underwriting capabilities, digitizing workflows, securing customer data or improving policyholder experience."

— Robert Pick, Group Deputy CITO, Tokio Marine (Carrier Management, March 2026)

That's the framing this entire post defends. The question is no longer "replace or keep." It's "where does new capital actually buy new capability?"

The buying behavior is finally catching up to a pattern that already won. Forrester projects US insurance tech spend will rise about 7.8% in 2026, to roughly $173 billion — and frames the shift bluntly: the story is moving "from modernization to intelligence." Spend is rotating away from rip-and-replace and toward embedding AI into existing processes.

The ecosystem data tells the same story. Guidewire's PartnerConnect marketplace surpassed 110 cloud-native integrations in early 2025, with partner-integration downloads up 32% year over year. By mid-2025, more than 75% of insurance firms had embedded APIs into their digital operations. Carriers aren't voting for destinations anymore; they're voting for ecosystems — for capabilities that plug into the core they already own.

Analysts even have a name for the pattern now. Datos Insights calls it the "skinny PAS" trend: keep the policy administration system focused on core transactional truth and push the differentiating, intelligence-heavy work to specialized layers around it. When the analysts give a pattern a name, the market has already moved.

Here's the framework in two halves.

Skinny PAS, Smart Edges

Skinny PAS — Keep the core thin. The policy administration system holds records, transactions, financials, and your regulatory state-of-truth. Don't over-customize it. Don't bend it to handle every edge case. Its job is to be stable, supported, and authoritative.

Smart edges — Put differentiation in the layers that touch the actual work: submission intake, document understanding, triage, enrichment, and broker communications. This is where intelligence belongs, because this is where the variability — and the cost — actually lives.

This is the same idea consultancies have been packaging as "composable architecture" and "Packaged Business Capabilities" — assemble modular, swappable capabilities around a stable core rather than monolithically rebuilding the core itself. The vocabulary differs; the conclusion is identical. The core is not where you win. The edges are.

It's also the cleaner way to think about digital transformation in insurance: transformation rarely fails because the core is too old. It fails because the work that surrounds the core — reading a broker's email, reconciling a loss run, keying an ACORD form — is still manual, and no amount of core replacement fixes that.

"Embeddable" is easy to say and easy to fake. In practice, it means the intelligence lands inside the tools your team already uses — and the underwriter never logs into anything new. Mapped to the document workflows every commercial carrier runs:

In every one of those workflows, the differentiator isn't a new screen. It's that the work happens where work already happens. That's the heart of intelligent document processing for insurance done right — and why pairing extraction with insurance-specific AI with human-in-the-loop review beats dropping a generic, autonomous tool into the middle of a regulated workflow.

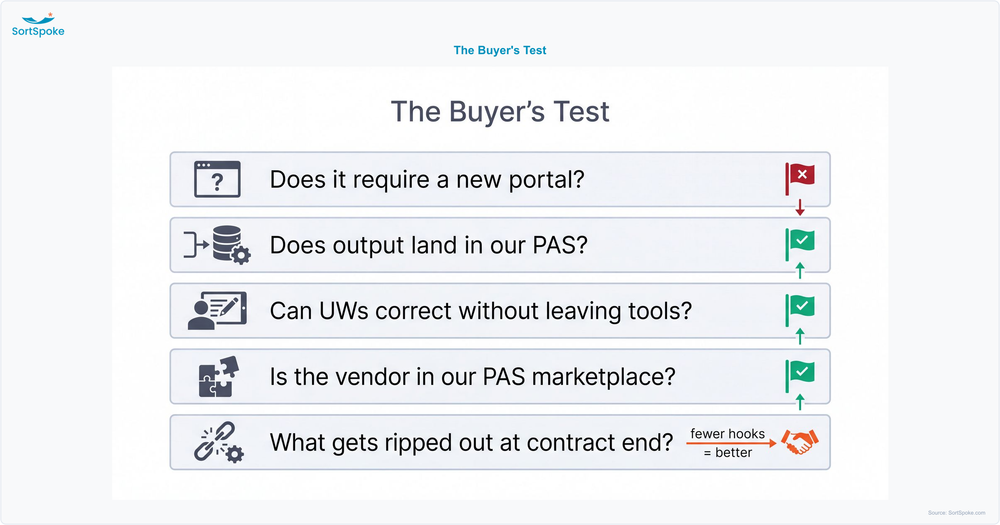

If you take one thing from this post to your next vendor evaluation, take this checklist. The first question is the whole game; the rest are how you pressure-test the answer.

Notice what these five questions quietly filter. A portal-first platform fails question one. An autonomous "agentic" tool that makes decisions in its own environment fails questions two and three. The test isn't anti-AI — it's pro-integration. It rewards AI that strengthens the workflow your team already trusts, and screens out AI that asks them to abandon it.

None of this means replacement is always wrong. It means replacement is overprescribed and embeddable AI is underprescribed — and the goal is to put each in its right place. Replacing the core is the right call when:

For most commercial carriers, though, none of those is the situation. The core works "modern enough." The bottleneck is at the edges — submission intake, loss runs, document workflows — where the manual cost is concentrated and where intelligence pays back fastest. Diagnosing which problem you actually have is exactly the kind of question worth working through with a partner; it's a recurring theme in our partnership with Burnie Group, whose consulting work centers on integrating intelligence into existing operations rather than ripping them out.

The upside of getting this right is not subtle. The ACORD 2025 Insurance Digital Maturity Study, which analyzed 210 of the world's largest carriers, found that only about a quarter have truly digitalized the value chain. ACORD estimates that robust AI integration could cut P&C expenses by as much as 14.6% — more than $480 billion in annual savings across the industry.

Read that alongside the failure data and the conclusion writes itself: the carriers capturing that value aren't the ones that finished a multi-year replacement. They're the ones that got intelligently integrated — adding capability at the edges without betting the core. You don't have to be "fully transformed" to win. You have to be connected where it counts.

If "smart edges" is the strategy, document workflows are where you start — because every modernization initiative, every AI roadmap, every "transformation" hits the document layer first. Submissions, loss runs, ACORD forms, SOVs: they're the universal on-ramp into the core, and they're almost always the most manual, most expensive part of the operation.

That makes automated document processing the highest-leverage first move. You modernize the document layer on top of the core you already have, capture a fast time-to-value win — months, not the years a replacement demands — and reinvest the savings in the next edge. It's also the most direct route to handle more submissions without headcount, because the capacity gain comes from removing manual re-keying, not from hiring.

This is precisely the model behind our Sapiens partnership: document AI that extracts and validates data and writes it back into the carrier's existing platform — no new portal, no parallel database, no rip-and-replace.

There's a final, underrated reason embedded beats replacement: it compounds, and it compounds immediately. Every document interaction logs an audit trail — a compliance win. Every underwriter correction trains the model — an accuracy win. Every broker handoff captures relationship intelligence — an operational win. The system gets measurably better the more it's used, starting in week one.

Replacement programs don't compound until they ship. And most don't ship — at least not on time, on budget, or with everything the old system did. The strategically lower-risk path isn't the one that promises a clean slate in five years. It's the one that's additive, removable, and improving today. That's the case for building intelligence at the edges, and it's the methodology we walk through in Our Approach.

If your AI vendor wants you to retrain your team on a new portal, you're being sold another system to integrate — not a solution to integration. Book a 15-minute demo → to see how SortSpoke embeds into the PAS your team already uses — whether that's Guidewire, Duck Creek, Sapiens, or another core — writing data back via API. No new portal. No new login. Just AI where the work happens.

Commercial P&C Insurers Guide to Solving the Underwriting Bottleneck

.png?width=500&height=300&name=Website%20Blog%20Images%20(20).png)