Insurance document processing automation is the missing link: Carriers have digitized portals and dashboards, but the document intake layer — where 80% of insurance data lives — remains manual, exception-heavy, and largely unchanged.

The document layer is a specific bottleneck: Intake, classification, extraction, and routing are where digital and manual workflows collide. Everything downstream depends on getting this right.

OCR and template-based tools have hit a ceiling: Insurance documents are too variable, too exception-prone, and too high-stakes for brittle automation. That's why so many AI pilots never scale.

Human-in-the-Loop is the resolution — not the workaround: Structured human correction trains AI over time, creates regulatory defensibility, and builds underwriter trust without requiring a rip-and-replace of existing systems.

Most insurance carriers will tell you their digital transformation is well underway. They have a modern submission portal. They have a data warehouse. They have a shiny analytics dashboard that leadership reviews every quarter. And yet, somewhere between the broker hitting "submit" and the underwriter opening a structured risk file, a team of people is still manually reading PDFs, copy-pasting numbers into spreadsheets, and chasing email threads for missing attachments.

That gap — between the digital front-end and the structured back-end — is what we call the document layer. And for most carriers, it is the specific point where insurance document processing automation has either never been attempted or has been attempted and quietly failed.

This isn't a technology problem, exactly. It's a sequencing problem. Carriers digitized the visible parts of the workflow first — the customer-facing portal, the reporting layer, the underwriting workbench — and left the messy, high-variation document processing in the middle as a people problem. The result: every downstream transformation is built on a foundation of manual extraction, and the cracks are starting to show.

Digital Transformation Has a Dirty Secret

When insurance executives talk about digital transformation, they usually mean a modernized quoting portal, a move to cloud infrastructure, an AI-assisted underwriting tool, or a revamped customer experience layer. These investments are real. But they share a common blind spot.

Only 18% of insurers say their workflows are fully automated. Meanwhile, 80% of insurance data is unstructured — locked inside PDFs, scanned documents, broker emails, and handwritten forms that no CRM or policy administration system can read directly.

That gap is not an accident. Organizations automate what is easy to automate first. Structured data flows, digital forms, API-connected systems — those get modernized. Unstructured document intake, with all its format variation, exception handling, and judgment calls, gets deferred.

The consequences compound quietly. Senior underwriters spend 60 to 70% of their day extracting and validating information from documents rather than assessing risk. Meanwhile, 66% of brokers say carriers must triage submissions faster — not as a nice-to-have, but as a competitive requirement, a dynamic the 2026 submission benchmarks capture across response time, appetite fit, and quote-to-bind. The cost is amplified by an industry-wide underwriting talent crisis that is shrinking the senior bench at exactly the moment volume and complexity are rising.

The front-end looks modern. The back-end stores clean data. But in the middle, the document layer is still operating the way it did fifteen years ago. Our companion post on digital transformation in insurance examines why these gaps persist even after significant technology investment.

What the Document Layer Actually Is

Before we can solve the problem, we need to name it precisely. The document layer is not simply "document management" in the file storage sense. It is a set of four interconnected processes that happen — or should happen — every time a document enters an insurance workflow.

The Four Stages of the Document Layer

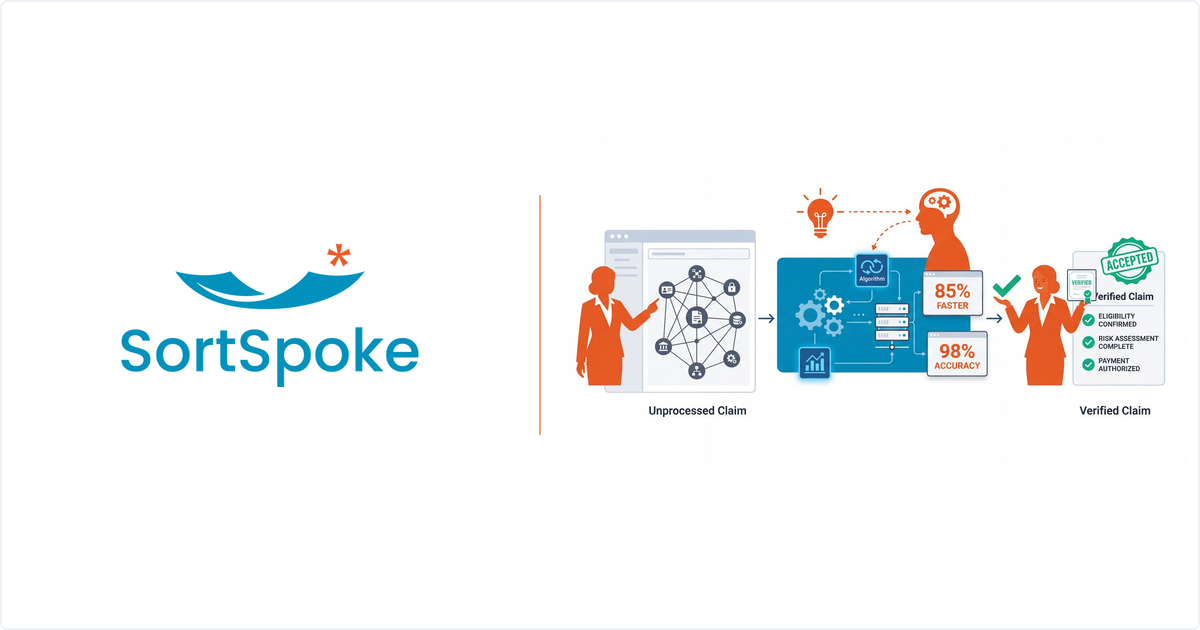

Intake: Receiving documents from multiple channels (email, portal upload, broker submission platforms, fax) and getting them into a processing queue without loss or duplication.

Classification: Identifying what type of document each file is — ACORD application, loss run report, statement of values, endorsement, policy, broker submission package — so it can be routed to the correct workflow.

Extraction: Pulling structured data fields from the classified document — insured name, policy number, coverage limits, loss history, premium — and translating them into a format that downstream systems can consume.

Routing: Directing the structured output to the right person, queue, or system — an underwriting workbench, a policy administration platform like Guidewire or Duck Creek, or a triage workflow for prioritization decisions.

Each stage looks simple in isolation. In practice, any one of them can break down in ways that stall the entire downstream workflow. A document classified incorrectly gets routed to the wrong queue. An extraction that misses a key field sends an underwriter on a manual search. A routing rule that can't handle a new document variant creates a backlog someone has to clear by hand.

For a broader view, our automated document processing guide covers the full landscape from basic OCR to modern AI. Our 2026 IDP guide provides the foundation on where the technology currently stands. And the document layer is also where submission triage begins — before an underwriter can prioritize which submissions to quote, the submission has to be understood.

Why Insurance Documents Are Uniquely Hard to Automate

It would be convenient if insurance documents behaved like invoices or purchase orders — standardized fields, consistent layouts, predictable formats. They do not. The insurance document ecosystem is one of the most complex unstructured data environments in any industry, for several compounding reasons.

Format Variability Is Not an Edge Case — It's the Norm

ACORD forms are nominally a standard, but any underwriter who has processed more than a few months of submissions knows the practical reality: every broker submits slightly differently. ACORD 125 comes in as a native PDF from one broker and a scanned photograph from another. Field positions shift. Supplemental schedules get appended in no particular order. Loss runs — a theoretically simple document type — come formatted according to whatever the prior carrier decided to call their columns.

Loss run variability alone is significant enough to warrant dedicated attention. Our posts on loss run automation and what loss run reports actually contain go deeper on the specific challenges of this document type — but the core issue applies across all submission documents: variation is not a bug in the ecosystem. It is a feature of how the broker market operates.

The Broker Ecosystem Amplifies Variation

A carrier processing commercial lines submissions may receive documents from hundreds of different brokerages, each with their own systems, templates, and submission habits. Some brokers use ACORD's online portal tools. Others use carrier-specific portals. Many still email PDFs assembled from multiple sources. The carrier has no control over how a document arrives — only over how they process it after it does.

For a deeper look at how this affects underwriting operations specifically, see our post on intelligent document processing for insurance, which covers the domain-specific challenges that make generic IDP tools underperform in this context.

Downstream Systems Demand Precision

Policy administration systems like Guidewire and Duck Creek are structured data environments. They have specific field schemas, validation rules, and data type requirements. When the document layer produces an extraction with a missing field, a wrong data type, or an ambiguous value, the downstream system either rejects the record or silently accepts something incorrect — and both outcomes create downstream costs.

This downstream precision requirement is what elevates the stakes. An extraction error in a low-stakes system is an inconvenience. An extraction error that propagates into a policy administration system can affect pricing, coverage terms, or regulatory reporting.

Where Automation Keeps Failing — And Why

The insurance industry has been attempting to automate document processing for decades. The tools have evolved — from basic OCR, to template-based extraction engines, to machine learning models — and the failure modes have evolved with them. Understanding the evolution from OCR to IDP to LLM-based extraction explains why each generation improved some things while leaving core problems unsolved. The practical pattern we hear repeatedly from underwriting and ops leaders: automation worked on easy cases, failed on hard cases, and the failures eroded confidence in the whole system.

OCR Was Never Built for This

Traditional OCR converts document images into machine-readable characters. It does not understand what those characters mean — whether a number represents a premium amount or a policy number, or how field relationships change across document variants. OCR accuracy degrades on scanned documents, handwritten annotations, merged table cells, and rotated text — all common in insurance. Layering extraction rules on top creates template-based systems that work on documents matching the template and fail unpredictably on everything else. In insurance, "everything else" is a large and growing category, which is why insurance-specific AI with human validation outperforms generic AI on the document types carriers actually receive.

Template Brittleness Creates a Maintenance Treadmill

Template-based systems require someone to define and maintain a template for each document variant. As brokers update their packages, carriers introduce new forms, and ACORD revises standards, templates break. The team patches the template — but the backlog has already accumulated, and the patch will break again on the next variant. Teams managing large template libraries often find themselves spending more time maintaining the automation than they saved by deploying it.

Trust Collapses After Early Errors

Perhaps the most persistent problem is not technical — it is organizational. When an automated system produces confident-looking output that turns out to be wrong, underwriters stop trusting it. A policy issued with a wrong limit because extraction got it wrong is not a minor quality issue. It is a liability.

Once trust collapses, the human review step gets applied to everything, not just the uncertain cases. The system still processes documents, but every output gets manually verified — which eliminates most of the efficiency gain and adds the cognitive overhead of verifying AI output on top of doing the work manually.

The data confirms this pattern. According to research we analyzed in our Trust Gap post, 78% of P&C insurers have experimented with AI in claims operations — but only 4% have scaled it meaningfully. A Wisedocs industry survey found that 54% of insurance professionals cite accuracy concerns as the primary barrier to adoption, and 44% cite a fundamental lack of trust in AI output. The technology isn't the bottleneck. Confidence is. For a view of what the intake process looks like when it's working correctly, what good submission intake looks like provides a useful benchmark.

The HITL Difference: Why the Human Isn't the Problem

The standard response to automation failures is to throw more humans at the exceptions — a larger review team, more QA steps, more escalation paths. This keeps the workflow moving but doesn't improve the underlying system, and it adds headcount cost that scales with document volume.

The alternative is to redesign the relationship between human reviewers and the AI so that human corrections make the system better over time. That's the core principle of Human-in-the-Loop AI — fundamentally different from treating humans as the backup plan when automation fails. We've explored why this matters at the strategic level in the $480M bet that humans still matter: the carriers compounding the largest gains are the ones who refused to automate the judgment layer.

Confidence Thresholds Change What Gets Reviewed

A well-designed HITL system doesn't route every document to human review. It uses confidence scores to flag which extractions need attention. High-confidence results pass through automatically. Borderline cases get flagged at the specific field level — not the entire document — so a reviewer can correct one value and move on in seconds, not minutes.

Human Corrections Train the AI — And Build Trust

Here's the stat that explains why this matters: trust in AI outputs jumps from 16% to 60% when human oversight is added — a 4x multiplier. Same AI, same outputs. The only difference is that a human verified the result. In mature HITL operations, correction rates typically run 10–20% in the first 90 days, then trend toward 5% or lower by six months as the model calibrates to your specific document types.

Every correction a human makes is a labeled training example. When a reviewer identifies that "GL Prem" in column three of a specific carrier's loss run means "general liability premium" — not a total figure — that correction improves extraction accuracy on similar documents in future runs. The AI gets better at the specific variants in your workflow, not just generic training categories. That's what separates HITL from simple human review: it's not just catching errors — it's systematically reducing the error rate over time.

"SortSpoke solves one of underwriting's messiest problems. Enables faster reviews, better risk assessment, greatly reduced manual effort."

— VP Underwriting, RGA

Explainability Supports Regulatory Defensibility

Regulators increasingly want to understand how AI systems make decisions that affect policyholders and pricing. A black-box extraction model with no audit trail creates compliance exposure. A HITL system creates a complete record: what the AI extracted, what confidence it assigned, whether a human reviewed it, and what correction was made. That audit trail is what allows a carrier to defend data quality in an examination and demonstrate that human judgment remained in the loop for consequential decisions. Our post on keeping humans in the driver's seat with insurance AI covers the organizational and regulatory dimensions in depth.

What "Solving the Document Layer" Actually Looks Like

The first instinct when fixing document intake is often to find a standalone platform that replaces the current workflow. This creates adoption risk — because the single biggest predictor of whether a document automation project succeeds is whether underwriters actually use it. Industry data shows that embedded tools see 3–5x higher adoption than standalone platforms. A tool that requires a new login is a tool that gets routed around. (BCG's research on AI-first insurers and the role of human oversight reaches the same conclusion from the strategy side: the gap between experimenting and scaling is structural, not technical.)

The answer is architecture, not features. Specifically, embeddable architecture — document AI that works inside the tools your team already uses, rather than requiring a new portal, a new login, or a new workflow.

No New Portal. No New Login.

When document processing lives inside the underwriting workbench, the submission queue, or the broker portal your team already works from, adoption isn't a change management project — it's a natural extension of how people already work. The output appears where it's needed. The review interface is already familiar. The friction of switching between systems disappears.

This is the practical meaning of "Document AI that meets your team where they already work." It's not a marketing phrase — it's a design requirement that determines whether the system actually gets used.

Structured Output Into Existing Systems

The end goal of the document layer is not a cleaned-up PDF or a summary report. It is structured, validated data in the schema that your downstream system expects. That means extraction outputs formatted for your specific Guidewire fields, your Duck Creek data model, your renewal workflow, or your triage queue — not a generic data format that requires another transformation step.

When the document layer produces outputs that downstream systems can consume directly, you eliminate an entire category of manual work: the re-entry, reformatting, and reconciliation that happens today between extraction and input.

Our IDP platform is built around this principle — structured output designed for the systems insurance teams actually run on. (For a broader walk-through of the evaluation criteria that hold up across maturity stages, see our insurer's guide to AI document extraction.)

Measuring Success: Metrics That Actually Matter

One of the consistent challenges in document automation projects is that teams measure the wrong things. They track documents processed per day, or hours saved on specific tasks, or vendor-reported accuracy rates on benchmark datasets. These metrics are real, but they don't tell you whether the document layer is actually performing.

The metrics that matter for insurance document processing automation are:

Straight-through processing (STP) rate: What percentage of documents flow from intake to structured output without requiring manual intervention? This is your headline metric. A low STP rate means you are still dependent on human effort for the majority of your volume. A high STP rate means automation is actually doing its job.

Exception rate by document type: Not all document types are equally hard to automate. Breaking down your exception rate by document type tells you where to focus improvement efforts and where your current model is weakest.

Time-to-structured-data: How long does it take from the moment a document is received to the moment structured data is available in the downstream system? This is the metric that directly affects underwriter response times and broker experience.

Correction rate over time: In a HITL system with a learning loop, your human correction rate should decrease as the AI improves on the specific document variants it encounters. If your correction rate is flat or rising over time, the feedback loop isn't working.

For a fuller diagnostic — including the operational signals that distinguish a working HITL deployment from one that is quietly failing — see 5 signs your HITL AI operation is working.

If you want to put numbers around the business case for improving these metrics at your organization, our ROI calculator helps translate STP rate improvements into specific cost and capacity impacts.

The Gartner Reality Check

Gartner research finds that 83% of data migration projects exceed budgets and timelines. A significant portion of that overrun traces back to data quality problems that originate at the document layer — unstructured inputs that weren't fully accounted for in the project scope. Solving the document layer before embarking on larger transformation projects reduces downstream project risk substantially. Deloitte's 2026 global insurance outlook reaches the same conclusion from the operating-model angle: the carriers winning on digital are the ones redesigning workflows, not the ones deploying the most technology.

Getting Started: What to Fix First

The scope of the document layer problem can feel paralyzing — a mix of document types, legacy system dependencies, and underwriters who have built workarounds around the current broken process. The good news is that you don't need to solve everything at once.

Start With High-Volume, Lower-Complexity Documents

Every carrier has document types that are high volume, relatively standardized, and not particularly high-stakes for individual extraction errors — things like ACORD 125 applications from brokers who consistently use the same format, or loss run reports from a small number of frequently used prior carriers.

These are the right starting point: they generate training data volume quickly, produce measurable STP rate gains without requiring the model to handle the full spectrum of variation, and build organizational confidence before the system encounters harder cases.

Build HITL Before You Scale

The most common mistake is deploying automation broadly before the correction loop is functioning. Teams scale volume through the system, discover errors accumulating faster than they can be corrected, and end up with a backlog of bad extractions and a system that hasn't learned anything. The shape of that correction layer is itself a design choice — we've outlined four ways to staff a human-in-the-loop operation based on volume, complexity, and how much of the work needs to live with the underwriter versus a dedicated review team.

The right sequence: deploy with a controlled document set, confirm corrections are feeding back into the model, validate improving accuracy before expanding volume. It feels slower in the first 60 to 90 days — but it produces a system that works at scale rather than one that gets rebuilt after the initial deployment fails. Carriers staring at growing submission volume can also reference our playbook on how to handle more submissions without adding headcount — the document layer is the single biggest lever for capacity expansion.

Our Underwriting Efficiency Calculator can help you model the capacity impact of improving STP rates at different stages of rollout, so you can build a realistic business case for the phased approach.

Frequently Asked Questions

What is insurance document processing automation?

Insurance document processing automation uses AI to handle the intake, classification, extraction, and routing of insurance documents — ACORD forms, loss runs, submission packages — without manual data entry. Effective automation produces structured outputs compatible with downstream systems like Guidewire or Duck Creek, reducing the time from document receipt to underwriter action.

Why do so many insurance document automation projects fail?

Most failures trace to three causes: template-based systems that break when document formats vary, AI models deployed without a correction loop to improve accuracy over time, or tools that require underwriters to adopt a new portal, which drives low adoption. Projects that address all three — flexible AI, structured HITL feedback, and embeddable architecture — have significantly higher success rates.

What is the difference between OCR and intelligent document processing for insurance?

OCR converts document images into machine-readable text. Intelligent document processing (IDP) adds classification, contextual extraction, and validation — understanding not just what characters are, but what fields mean across different layouts. For insurance, IDP also incorporates domain knowledge about ACORD forms, loss runs, and submission package structures.

How does Human-in-the-Loop improve insurance document automation over time?

In a HITL system, human reviewers correct low-confidence extractions. Those corrections feed back into the AI model as labeled training data, improving accuracy on similar documents in future runs. Over time, the correction rate decreases as the model becomes more accurate on your specific document variants — without manual template maintenance.

Which insurance documents should be automated first?

Start with high-volume, relatively consistent document types within your broker relationships — ACORD applications from top submission sources, loss runs from frequent prior carriers, or policy declarations for a specific line. These generate training volume quickly, produce measurable STP rate gains, and build organizational confidence before tackling higher-variability types.

Key Takeaways

1

The document layer — intake, classification, extraction, and routing — is the specific point where most insurance digital transformations stall. Every downstream system depends on it, but most carriers still operate it manually or with brittle template-based tools.

2

OCR and template-based automation have hit a ceiling in insurance because document variability, broker ecosystem complexity, and downstream precision requirements exceed what those tools can reliably handle. The path forward requires AI that handles variation natively, not templates that must be rebuilt with every format change.

3

Human-in-the-Loop architecture is not a fallback for when automation fails — it is the mechanism by which automation improves. Human corrections create a feedback loop that raises accuracy on your specific document variants, builds regulatory defensibility, and earns the underwriter trust that determines whether the system actually gets used.

4

Start with high-volume, lower-variability document types to generate training data and build organizational confidence before expanding scope. Build the HITL correction loop before scaling volume — teams that skip this step end up rebuilding their systems after the initial deployment underperforms.

See What the Document Layer Looks Like When It's Solved

If you're dealing with manual intake bottlenecks, exception-heavy extraction workflows, or AI pilots that never moved to production — the document layer is the right place to start. We work with insurance carriers and MGAs who have exactly these challenges.

.png?width=500&height=300&name=Website%20Blog%20Images%20(20).png)